Kenya removes excise duty and stamp requirements for bottled water effective 1 July 2026.

6 July 2026

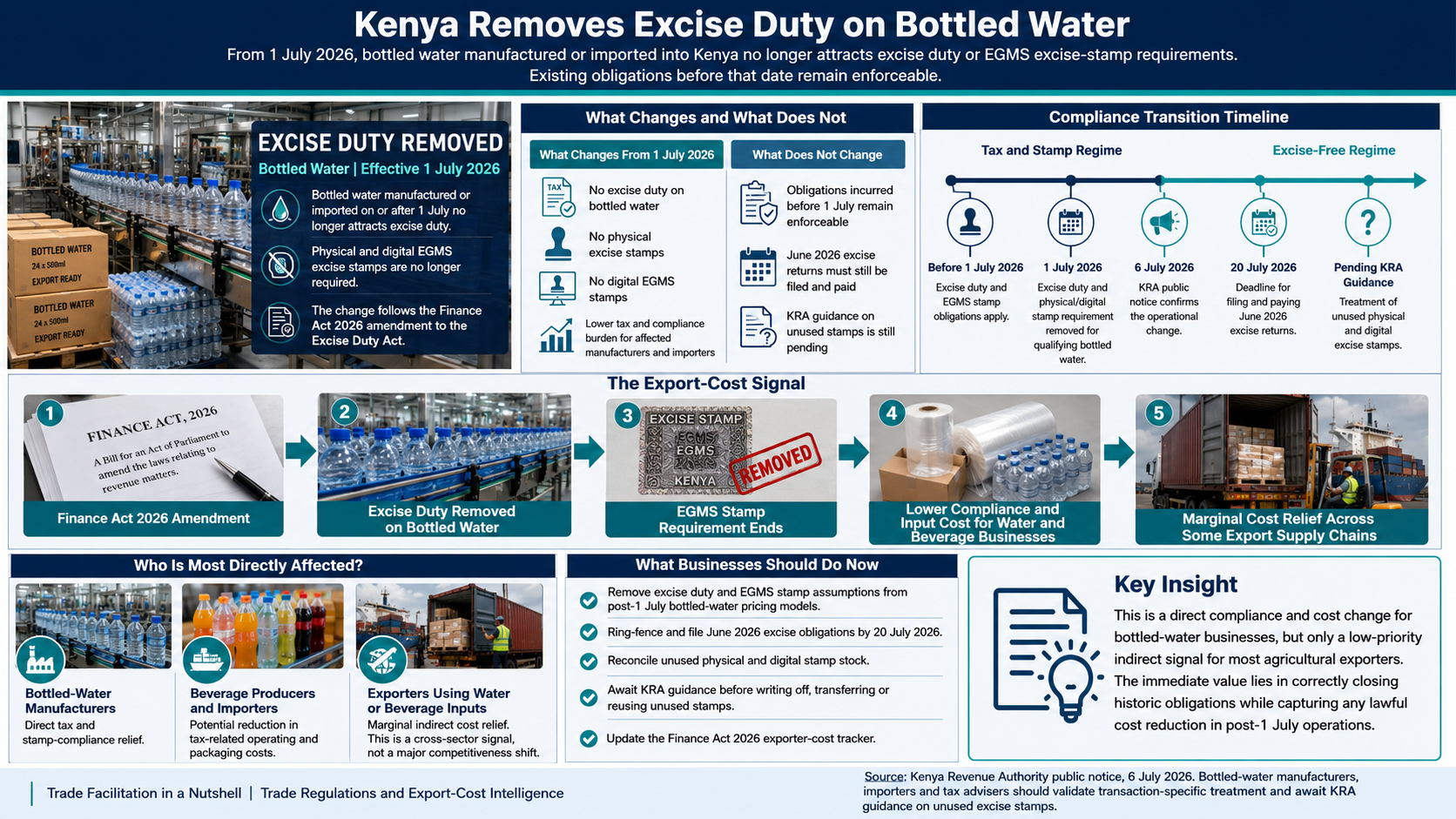

Kenya has removed excise duty and excise-stamp requirements for bottled water manufactured or imported from 1 July 2026. The policy change creates a direct tax and administrative relief for bottled-water manufacturers and importers, while its implications for most horticulture, logistics and manufacturing exporters are limited. The operational priority is to separate post-effective-date treatment from enforceable pre-1 July obligations, file June 2026 excise returns by 20 July, and preserve unused stamps pending KRA guidance.

By Beryl Njeri OlubandwaTrade Facilitation in a Nutshell

Share:

inXf

KEY TAKEAWAY

The removal of excise duty and EGMS stamps is a material change for the bottled-water value chain but should not be mistaken for a broad reduction in export costs. Businesses must prioritize closing June 2026 obligations while awaiting official guidance on unused stamp inventory.

Introduction

The Kenya Revenue Authority has confirmed that, following the Finance Act 2026, excise duty and EGMS stamp requirements for bottled water are removed for all products manufactured or imported from 1 July 2026. This policy shift offers direct administrative and tax relief to specific value chains while maintaining strict enforcement of pre-existing obligations. Exporters should treat this as a category-specific update rather than a systemic shift in the national cost of trade.

By the numbers

1 July 2026

Effective date of excise removal

20 July 2026

Deadline for June excise returns

Zero

New excise duty rate for bottled water

Pending

KRA guidance on unused excise stamps

1

Operational Ticks

Direct benefits for the bottled-water value chain.

Why it matters

✓Elimination of excise duty on qualifying bottled water.

✓Removal of physical and digital EGMS stamp requirements.

✓Simplified compliance trail for post-1 July production and imports.

2

Compliance Risks

Common pitfalls in managing the transition period.

!Mistaking the policy for a retroactive tax amnesty.

!Failing to file and pay June 2026 obligations by the 20 July deadline.

!Prematurely disposing of or reusing unused excise stamps.

!Applying the relief to non-qualifying beverage categories.

!Assuming a material reduction in general export logistics costs.

Infographic

A compliance transition timeline illustrating the cut-off between pre-July obligations and the new excise-free regime for bottled water.

Long-form analysis

Navigating the bottled water excise transition

The Commercial Context

Tax changes only create value when they affect a material cost item, a binding compliance step or a commercial decision. This notice does all three for the bottled-water value chain, but not for every exporter. Its direct effect is the removal of excise duty and stamp requirements for a specified product category from a specified effective date. The operational consequence is a narrower tax burden and fewer excise-control steps on qualifying bottled-water transactions after 1 July 2026.

The weak logic would be to describe this as a broad easing of Kenya’s export-cost environment. Bottled water is not a universal input into horticulture, tea, coffee, cut flowers, apparel, leather, logistics or general manufacturing. Unless an exporter manufactures, imports, resells or uses bottled water at material scale, the impact on unit export cost will be immaterial. The notice should therefore sit in the Finance Act 2026 tracker as a category-specific cost signal, not as evidence that the wider burden of taxes, levies, permits, freight or packaging has fallen.

The date boundary matters. A post-1 July bottled-water transaction may qualify for the new treatment, but that does not remove historic obligations. A business that treats the new position as retroactive risks a missed return, an incorrect reconciliation or unsupported treatment of stamps. The better operating model separates transactions by manufacture or import date and closes June obligations before reconfiguring the future-state process.

What the Notice Changes, and What It Does Not

The notice described in this update sets out two changes for bottled water manufactured or imported on or after 1 July 2026: excise duty is removed, and physical or digital EGMS excise stamps are no longer required. This is both a tax and compliance change. It may reduce cash outflow, eliminate stamp-ordering and reconciliation tasks, and simplify the evidence trail attached to qualifying bottled-water transactions.The scope is equally important. The notice does not justify a general claim that all beverages, all packaging materials, all water-related inputs or all export products have become cheaper. It also does not remove the need to comply with other product, quality, customs, food-safety, VAT, import or business requirements that may apply. Companies should read the policy exactly as written: a product-specific excise and stamp change, with a defined effective date and explicit treatment of pre-effective-date obligations.

Why This Is Low Priority for Most Exporters

The competitive relevance for most exporters is limited for three reasons. First, bottled water is usually not a core production input. Second, excise duty is removed only for the bottled-water product scope captured by the notice. Third, no reliable impact estimate should be asserted without the company’s actual product mix, transaction values, procurement pattern and tax treatment. A generic statement that the change will materially reduce export costs would be weak and hard to defend.

There are, however, specific cases where the change may matter. A business producing bottled water for domestic or export sale has direct margin and pricing exposure. An importer or distributor of bottled water has clearance and stamp-process exposure. A hotel, caterer, airline-service provider, event operator, employer or exporter that purchases bottled water at high volume may see a small indirect consumables effect. The correct question is not whether the notice affects “exporters” in general. It is whether bottled water is a material revenue line, purchased commodity or compliance category for the individual business.

This distinction protects management from two common failures. The first is false optimism, where a narrow tax relief is translated into an inflated margin assumption. The second is operational drift, where a business fails to close June liabilities because teams focus only on the apparent future saving. Both can be avoided through a short applicability test, a dated transaction reconciliation and a documented decision on whether the policy change is commercially material.

Direct and Indirect Exposure by Business Type

Bottled-water manufacturers and brand owners are the primary beneficiaries. They should model the removal against each qualifying SKU, revise their tax configuration, reconcile stamps, reassess invoice treatment and make a deliberate decision on how much of the benefit is retained as margin or passed through to distributors and customers. Importers of bottled water require a parallel import-control review: post-effective-date entries may no longer need excise stamps, but the import date, commodity description and documentation must support the treatment.

For non-water exporters, the likely impact is second order. Firms should only update cost assumptions after confirming that bottled water forms a recurring and material category in staff provisioning, client hospitality, buyer-service operations, sales bundles, transport services or another specific line item. The analysis should not assign a saving to packaging, cartons, bottles, labelling, freight or agricultural inputs unless there is a direct causal link to the excise change. That discipline matters because a cost tracker is useful only when it distinguishes confirmed savings from background policy noise.

The Wider Signal for Kenya’s Export-Cost Environment

The broader signal is not the monetary size of this one change. It is the need for exporter-facing businesses to translate Finance Act amendments into transaction controls quickly. Policy reforms are often announced at a high level, but commercial impact depends on product coverage, effective dates, stock held, tax system configuration, import documentation and responsibility across finance, operations, procurement and clearing agents.A well-run exporter-cost tracker converts each notice into four decisions: what changed, who is directly affected, what must be closed from the old regime, and whether the impact is material enough to change a price, budget, contract or operating procedure. For unrelated exporters, this notice normally fails the materiality test. It is low priority, not irrelevant.

How to adopt this immediately (Subscribe)

Finance Act 2026 Exporter-Cost Tracker

Excise Change Applicability Checklist

Excise Stamp Transition Log

Tax Change Communication Note

Call to Action / Integration: How to use this immediately

How TFN will support you

TFN provides the tools to ensure your business remains compliant while avoiding unnecessary administrative overhead.

Detect: track Finance Act notices, effective dates and implementation guidance that could change costs or controls.

Diagnose: establish direct product exposure, indirect exposure, legacy tax risk, stamp exposure or no material exposure.

Decide: quantify only verified cost or compliance effects and disregard background policy noise

Deploy: turn the response into a checklist, tracker entry, stamp log, internal note and management cadence.

Kenya removes excise duty and stamp requirements for bottled water effective 1 July 2026. | Trade Facilitation Blog