Kenya's new local marine cargo insurance rule turns Incoterms into a critical input-clearance risk.

3 July 2026

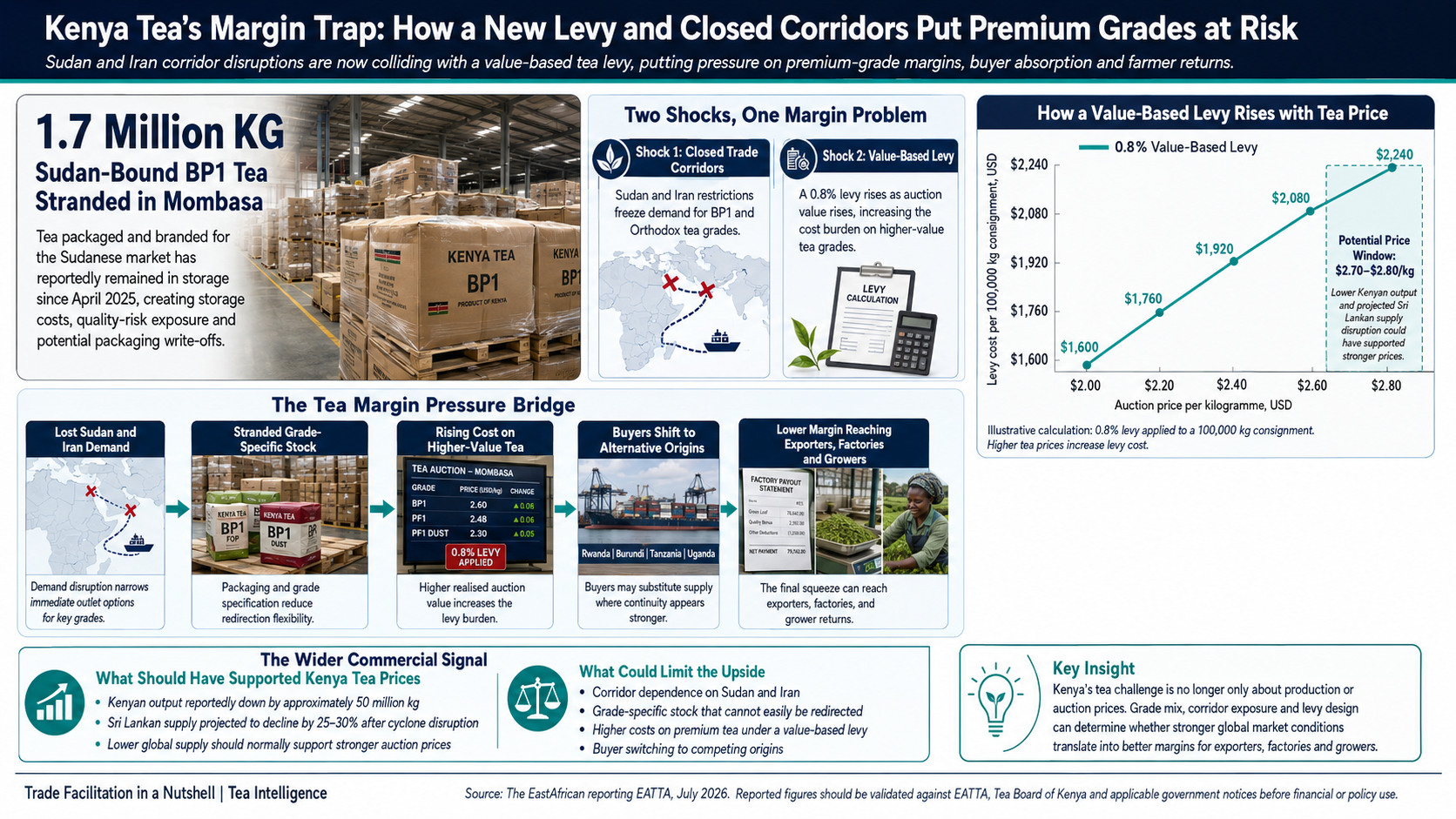

Kenya’s tea sector is facing a new margin squeeze. As 1.7 million kg of Sudan-bound BP1 tea remains stranded in Mombasa, a value-based levy is adding pressure to premium grades just as tighter global supply could have supported stronger prices. This analysis examines what lost corridors, buyer switching and levy design could mean for exporters, factories and growers.

By Beryl Njeri OlubandwaTrade Facilitation Director

Share:

inXf

KEY TAKEAWAY

The new requirement to use locally licensed marine insurance for Kenyan imports necessitates an immediate shift in procurement strategy. Importers must move away from 'CIF' terms to avoid duplicate insurance costs and clearance bottlenecks.

Introduction

As of 1 July 2026, all imports destined for Kenya require marine cargo insurance issued by a locally licensed provider, digitally verified through the KRA's iCMS platform. This shift moves a vital compliance responsibility from foreign suppliers directly to the Kenyan importer. Failure to align contract terms with this new digital verification workflow risks significant production stoppages and increased landed costs.

By the numbers

1 July 2026

Effective date of local insurance mandate

iCMS

Digital platform for verification

CFR

Recommended Incoterm for importers

High

Risk level for time-critical inputs

1

Strategic Compliance Ticks

Actions that ensure your supply chain remains resilient under the new regulatory framework.

Why it matters

✓Transitioning supplier contracts from CIF to CFR to eliminate duplicate insurance coverage.

✓Establishing a direct, verified link between local insurers and the KRA customs system.

✓Updating landed-cost models to account for locally sourced insurance premiums.

2

Operational Risk Factors

Common pitfalls that can lead to cargo detention and increased demurrage costs.

!Ignoring cargo already in transit that lacks a locally issued certificate.

!Assuming foreign suppliers will automatically adjust their CIF pricing.

!Failing to integrate insurance verification into the pre-clearance checklist.

!Overlooking the impact of insurance certificate delays on production-critical inputs.

!Lack of coordination between clearing agents and local insurance providers.

Infographic

A visual workflow mapping the transition from foreign-led CIF insurance to a locally verified iCMS-compliant clearance process.

Long-form analysis

Navigating the New Marine Insurance Compliance Landscape

The Commercial Context

Kenya’s tea sector is facing two pressures at the same time: important traditional markets have become commercially inaccessible, while a new levy structure is reportedly weakening buyer absorption at a moment when the sector expected stronger prices.The clearest sign of the market-access problem is in Mombasa, where approximately 1.7 million kilogrammes of BP1 tea packaged and branded specifically for Sudan have reportedly remained stranded in warehouses since April 2025. More than a year later, the stock continues to attract storage costs, faces growing quality risk, and may require the original Sudan-specific packaging to be written off.

At the same time, the value-based 0.8% tea levy introduced in May 2026 has added a second layer of pressure. Unlike a per-kilogramme charge, a levy calculated as a percentage of sale value rises as tea prices rise. This means premium grades may carry a proportionately higher charge precisely when exporters, factories and growers should be able to benefit from improved market prices.The issue is therefore bigger than a single levy or a single stranded consignment. It is a commercial warning about how market access, grade mix, buyer demand, pricing and policy design are now interacting across Kenya’s tea value chain.

How the Pressure Has Built Up

The Sudan disruption did not happen in isolation. Sudan and Iran have historically been important markets for particular Kenyan tea grades, including BP1 and Orthodox tea. When these corridors became closed or commercially constrained, stock prepared for those markets could not automatically be redirected elsewhere.Tea is not fully interchangeable once it has been graded, blended, packed and branded for a defined destination. A buyer in a different market may require another grade profile, pack size, label design, flavour preference, pricing arrangement or payment structure. This means a closed market does more than reduce demand. It can lock stock into a commercial format that is harder and more expensive to move.

The levy has reportedly amplified this pressure. EATTA has raised concern that a value-based levy can make Kenyan tea less attractive to buyers at auction when comparable supply is available from neighbouring origins. Rwanda, Burundi, Tanzania and Uganda have been cited as markets where absorption has remained substantially stronger.This is significant because the wider supply outlook should, in principle, have favoured Kenya. Kenyan output is reported to have fallen by around 50 million kilogrammes, while Sri Lankan production is projected to decline following cyclone-related disruption. Under normal market conditions, lower supply from major origins could support stronger prices. Kenya risks missing part of that upside if buyers perceive its tea as more expensive or less commercially predictable than competing supply.

What This Could Mean for Exporters, Factories and Growers

The immediate impact will not be the same for every business. Exporters with direct exposure to Sudan, Iran or other constrained corridors may carry the greatest burden through stranded stock, storage costs, unrecoverable packaging expenditure and working-capital pressure. Businesses with a heavier share of premium grades may also feel a value-based levy more sharply because the charge increases as sale values improve.For factories and growers, the concern travels further through the chain. When buyer absorption softens, the impact can affect auction confidence, stock levels, pricing expectations and eventually the value available to producers. A market that appears strong on paper can still underperform commercially if buyers pull back, delay purchases or switch to alternative origins.

There is also a buyer-confidence dimension. Buyers do not make sourcing decisions on quality alone. They assess price competitiveness, supply consistency, route reliability, product availability, payment confidence and the ease of completing transactions. Where competing origins appear simpler or more predictable, even a relatively modest cost difference can influence purchasing behaviour. The wider risk is not only lower sales into one market. It is that Kenya’s higher-value grades become more exposed at the point when global supply conditions should have created a stronger commercial opportunity.

The Wider Signal for Kenya’s Tea Sector

This situation shows why tea-sector competitiveness cannot be assessed only through production volumes, auction prices or headline export earnings. The sector’s performance also depends on whether key markets remain accessible, whether policy charges are commercially workable, and whether exporters can respond when a destination market becomes unavailable.

The current pressure should be treated as a sector-wide signal, not as a problem confined to a small group of exporters with Sudan-bound stock. It raises broader questions about how Kenya protects premium grades, manages dependence on vulnerable trade corridors and sustains buyer confidence when commercial conditions shift quickly.

The central point is straightforward. Kenya may have an opportunity to benefit from tighter global tea supply, but that opportunity will not automatically translate into stronger returns. The sector’s ability to convert lower supply into higher export value will depend on whether buyers continue to see Kenyan tea as competitively priced, reliable and commercially viable across multiple markets.

Subscribe to get the in-depth analysis

What happened and why it matters

What this means in practice for input-dependent exporters and manufacturers

Why this is a trade facilitation, contract and working-capital issue

The commercial pivot: stop treating Incoterms as boilerplate

What good looks like over the next 30 days

Strategic Rational

Consulting Playbook lens

How to adopt this immediately (Subscribe)

For freight forwarders, clearing agents and logistics providers • Build a pre-clearance check that confirms the local marine ….

For freight forwarders, clearing agents and logistics providers Build a pre-clearance check that confirms the local marine ….

Call to Action / Integration: How to use this immediately

How TFN will support you

Work with TFN: Do not wait for a critical packaging, fertiliser, agrochemical or machinery shipment to be held at clearance. Use the new requirement to strengthen the contract-to-clearance system now, while the transition can still be managed deliberately.

Detect: track policy changes, customs-system implications, insurer readiness and industry concerns that can affect import clearance.

Diagnose: identify whether the risk sits in contract terms, insurance coverage, certificate timing, digital verification, customs handover or input criticality.

Decide: select the right response, such as a CFR conversion, certificate escalation, cost-model update, supplier amendment or transaction exception plan.

Deploy: turn the response into checklists, SOPs, risk registers, supplier templates and management dashboards that teams can use immediately.

Kenya's new local marine cargo insurance rule turns Incoterms into a critical input-clearance risk. | Trade Facilitation Blog